The ECB Hits Pause but the Risks Are Rising

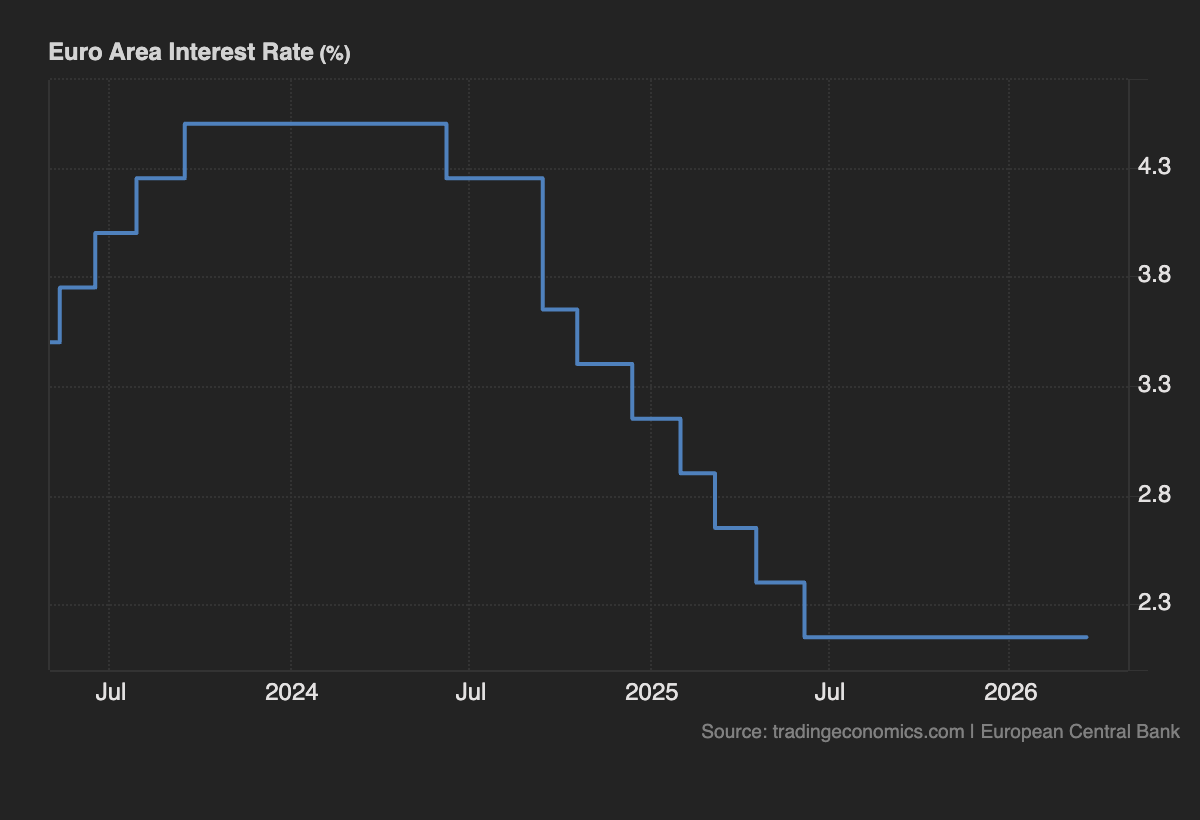

The European Central Bank held interest rates steady at its March 2026 meeting, signalling a cautious stance as global uncertainty continues to rise. Policymakers reaffirmed their commitment to bringing inflation back to the 2% target over the medium term, while acknowledging that the path ahead has become increasingly complex.

Interest rates remain unchanged, with the main refinancing rate at 2.15%, the deposit facility at 2.0%, and the marginal lending rate at 2.4%. This decision reflects a balancing act between controlling inflation and supporting an economy facing growing external pressures.

A key factor influencing the ECB’s outlook is the ongoing Middle East war, which has introduced significant uncertainty into the global economic landscape. The conflict has driven energy prices higher, creating renewed upward pressure on inflation while simultaneously weighing on economic growth. As a result, the ECB now sees greater risks on both sides, with inflation potentially remaining elevated for longer and growth slowing more than previously expected.

Updated projections highlight this shift. Headline inflation is now expected to reach 2.6% in 2026, before easing to 2.0% in 2027 and 2.1% in 2028. Core inflation forecasts have also been revised higher, indicating that underlying price pressures remain persistent beyond just energy related factors.

At the same time, the growth outlook has weakened. The ECB now forecasts GDP growth of 0.9% in 2026, rising modestly to 1.3% in 2027 and 1.4% in 2028. The impact of higher commodity prices, reduced real incomes, and softer confidence is expected to weigh on economic activity, particularly in the near term.

For investors and market participants, this paints a clear picture of the challenge ahead. The ECB is navigating a delicate environment where inflation risks remain elevated, yet growth momentum is fading. This tension suggests that policy is likely to remain restrictive for longer than some had anticipated, even as economic conditions soften.

Ultimately, the central bank’s latest decision reinforces a key theme for 2026. The era of straightforward disinflation is over, replaced by a more complex environment shaped by geopolitical risks and structural pressures.